SpaceX is no longer just an object of IPO speculation. On May 20, 2026, Space Exploration Technologies Corp. filed a Form S-1 with the U.S. Securities and Exchange Commission, beginning the public paper trail for what could become the largest initial public offering ever attempted.

The amended offering terms turned the story into a number large enough to feel unreal: 555.6 million Class A shares, an expected $135 share price, and roughly $75 billion raised before any underwriter option is counted.

At that price, SpaceX would enter public markets at a valuation near $1.77 trillion. That is the real subject of the IPO. Not whether Falcon 9 lands on drone ships. Not whether Starship eventually flies often enough to change heavy lift. The question is whether one company can make public investors pay today for launch, broadband, artificial intelligence infrastructure, and a Mars project whose costs could stretch for generations.

The filing changed the article from rumor to prospectus

The original version of this story treated a SpaceX IPO as theoretical. That is no longer accurate. The SEC filing exists, and the company has moved from private-market guessing into the formal machinery of a public offering.

A free writing prospectus filed with the SEC on June 3 pointed investors back to the preliminary prospectus and its amendments, the kind of paper trail that separates market chatter from an offering process.

That does not mean the final trade has happened yet. The offer price can still be finalized, demand can still shift, and public-market trading can still behave differently from the roadshow. But the central fact is now clear: SpaceX has filed, and the IPO story is no longer a purely speculative secondary-market exercise.

The scale is what makes it historically strange. Business Insider reported that the offering would raise about $75 billion, more than twice the $29 billion raised by Saudi Aramco in 2019. The Guardian described the shares as poised for release on June 12, with 555.6 million shares expected to be sold.

Why the $1.77 trillion price is not really about rockets

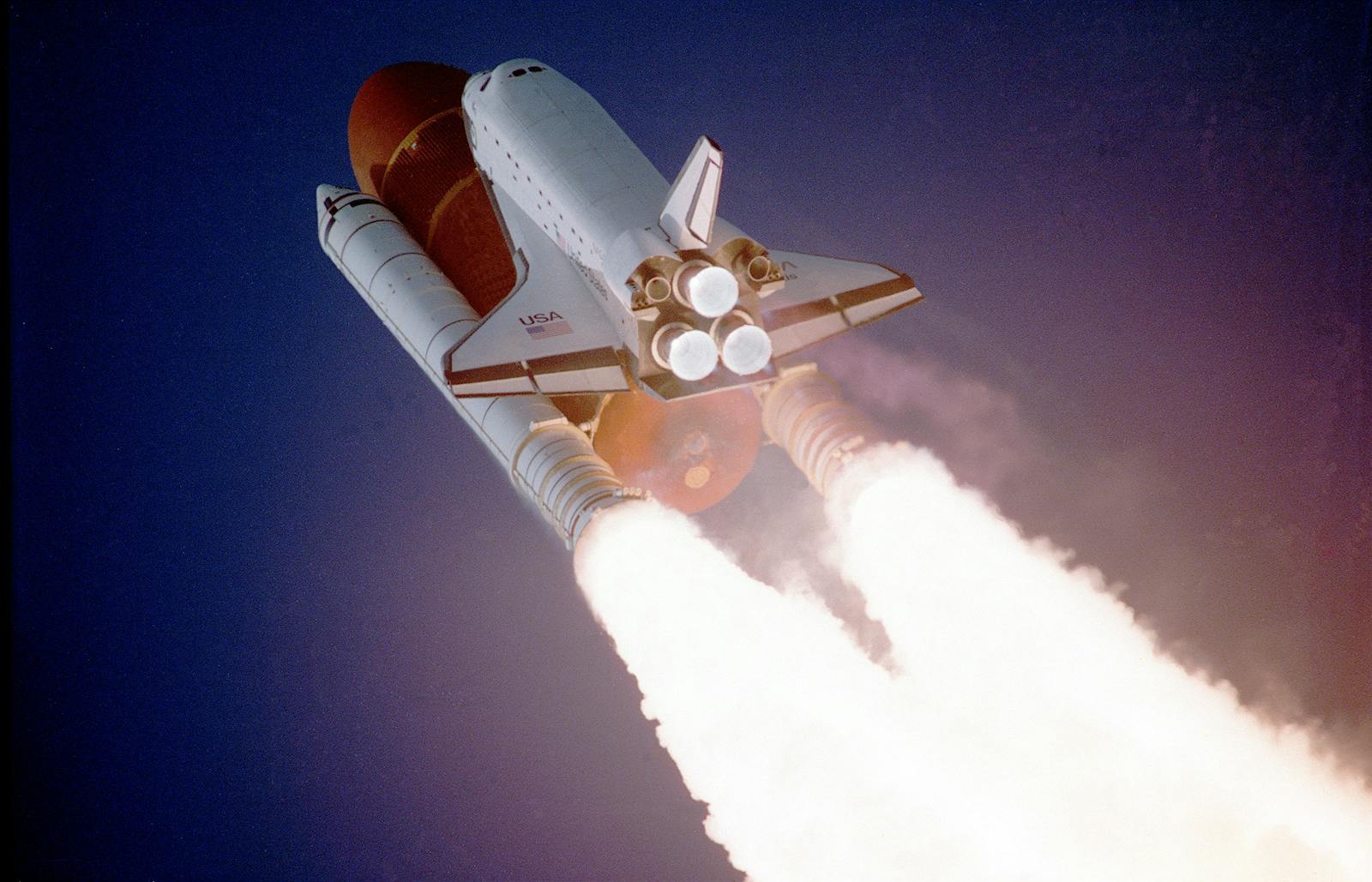

SpaceX’s rocket business is real. Falcon 9 turned booster landing from spectacle into operating rhythm, and Dragon made the company central to NASA’s human spaceflight supply chain. NASA describes Crew-9 as the tenth crewed Dragon flight under the Commercial Crew Program, launched on September 28, 2024, for a mission to the International Space Station.

But rockets alone do not explain a trillion-dollar-plus IPO valuation. Launch is hardware, scheduling, regulation, fuel, pads, weather, range safety, and failure risk. It can be lucrative, but it is not usually priced like a global software platform.

The valuation depends on the stack SpaceX has built around launch. The company designs rockets, launches payloads, manufactures satellites, operates Starlink, sells connectivity, and now asks investors to consider AI infrastructure as part of the same machine.

That is why an earlier SpaceDaily analysis of Starlink’s role in the valuation remains central to the IPO. Starlink is not a side project inside the story. It is the recurring-revenue engine that makes the rocket company look, to bullish investors, like a communications and infrastructure platform.

Starlink is the cash engine investors can actually see

The strongest version of the SpaceX bull case starts with Starlink. The satellite internet network gives SpaceX something launch companies historically lacked: a large consumer and enterprise service that can produce recurring revenue after the rocket has left the pad.

Via Satellite reported that the S-1 showed $18.7 billion in 2025 revenue, with Starlink as the largest revenue driver, while the company still posted a $4.9 billion net loss. That combination is the whole tension of the IPO in one sentence: a giant operating machine, still consuming more money than it returns on a GAAP basis.

Starlink also changes the meaning of SpaceX’s launch cadence. Every Falcon 9 launch that adds satellites to the constellation is not only a launch services event. It is also capacity expansion for the broadband network SpaceX owns.

That is the vertical integration investors are being asked to value. SpaceX does not merely buy launch capacity from someone else, then operate satellites at the mercy of another provider’s manifest. It owns the rocket, the satellite factory, the constellation, and the customer relationship.

The AI layer is where the valuation becomes speculative

The most aggressive part of the IPO story is not Starlink as broadband. It is Starlink, launch, and SpaceX’s infrastructure being folded into a future where AI compute becomes part of the company’s addressable market.

That is also where the claim becomes hardest to price. Data centers in orbit, AI infrastructure tied to satellite networks, and compute capacity treated as a space asset are not yet mature public-market businesses. They are strategic possibilities with enormous capital requirements.

Business Insider reported that SpaceX’s S-1 disclosed major AI-related details after the company’s integration with xAI, including heavy capital expenditures around compute. Those disclosures help explain why the valuation is not just about rockets, even if rockets are still the machinery that makes the rest physically possible.

This is the same dependency that makes Starship matter. Falcon 9 can keep launching Starlink satellites, crew capsules, cargo missions, and government payloads. But the larger future SpaceX is selling depends on Starship becoming operational at a scale Falcon 9 cannot match. A separate SpaceDaily report on Starship’s next-generation role noted that larger Starlink satellites, orbital data center concepts, science payloads, and eventual Mars cargo missions all assume a reusable heavy-lift system beyond Falcon 9’s limits.

The loss matters because the IPO is selling the future

The phrase “still losing money” should stay in the article, but it needs precision. SpaceX is not a small startup burning cash before product-market fit. It is a massive infrastructure company with real revenue, real government contracts, real broadband customers, and a reported multibillion-dollar net loss.

That distinction matters. A $4.9 billion net loss in 2025 does not mean the rocket business is fake or Starlink has no value. It means public investors are being asked to fund a company that is still in expansion mode while also absorbing the costs of AI infrastructure and long-horizon space ambitions.

SpaceX’s stated mission also changes the investor bargain. The company has long framed its purpose around making life multiplanetary, a goal that does not fit neatly into quarterly earnings culture.

For a public shareholder, that creates a strange compact. The same founder-driven mission that helped SpaceX build reusable rockets and the world’s dominant satellite broadband network may also direct capital toward Mars hardware, Starship infrastructure, and AI systems whose payoff is distant or uncertain.

Control is part of what buyers are really buying

The IPO also gives public investors economics without ordinary influence. The Guardian reported that Elon Musk would retain 82.4% of the voting power after the offering. MarketWatch similarly described a structure in which Class B shares carry far greater voting power than the Class A shares sold to the public.

That governance structure is not incidental. It means buyers are not only valuing launches, Starlink, AI infrastructure, and Mars. They are also buying into Musk’s continued control over how those pieces are prioritized.

This makes the IPO less like a normal aerospace listing and more like a public vote on a founder’s industrial map. The rocket pads in Florida, the Starlink dishes on rooftops, the Starship towers in Texas, the data centers, the Mars drawings, and the SEC filing all sit inside the same proposed security.

That is why the $1.77 trillion figure feels so large. It is not the price of a rocket company. It is the price of asking public investors to believe that the same machine that lands boosters at sea can also become a broadband utility, an AI infrastructure provider, and the transport layer for a civilization-sized project that has not yet left Earth.